Breaking News

Business

Methane Is the Elephant Metrics for O&G, agriculture and waste you must not ignore.

Methane has become the “elephant in the room” of climate policy—an issue too large to ignore yet still under-addressed compared to carbon dioxide. While CO₂ often dominates corporate disclosures and government pledges, methane is far more potent as a greenhouse gas in the short term, trapping more than 80 times the heat of carbon dioxide over a 20-year period. This means that reductions in methane emissions can deliver rapid climate benefits, making accurate measurement and management critical for industries such as oil and gas, agriculture, and waste management.

In the oil and gas sector, methane leakage occurs throughout the value chain—from drilling and extraction to processing, transmission, and distribution. Historically, reporting relied on estimates rather than direct measurements, leading to significant understatements of actual emissions. Today, the metrics that matter include leak detection and repair (LDAR) frequency, measured leakage rates per unit of output, and total volumes of “flared vs. vented” gas. Satellite-based monitoring and advanced sensors are now transforming the accuracy of these disclosures, giving investors and regulators clearer insight into whether companies are genuinely addressing the problem or simply relying on outdated assumptions.

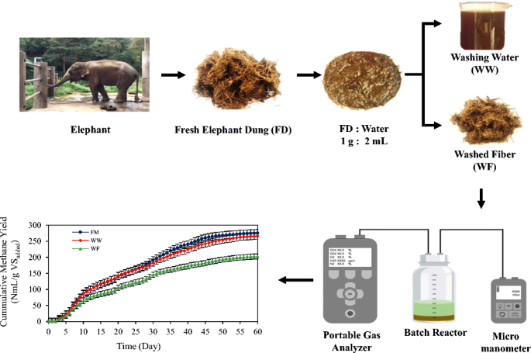

In agriculture, methane emissions are dominated by livestock and rice cultivation. Key metrics here include emissions intensity per unit of meat or milk produced, the adoption of feed additives to suppress enteric fermentation, and the scale of methane capture from manure management systems. Countries and companies that have begun publishing farm-level data are setting a precedent for accountability, but challenges remain in standardizing methodologies across regions with vastly different agricultural practices. For food companies and retailers, tracking supply chain methane footprints is becoming as critical as monitoring carbon.

In the waste sector, methane is primarily released from landfills and wastewater treatment. The most important indicators involve the proportion of waste managed through methane-capture systems, the efficiency of gas-to-energy conversion projects, and reductions in uncontrolled landfill emissions. With urban populations growing, waste-related methane is projected to rise unless systematic mitigation strategies are embedded into municipal and corporate operations.

The common thread across these sectors is the need for transparent, verifiable, and comparable methane metrics. Without them, investors cannot assess climate risk exposure, regulators cannot enforce effective policy, and companies risk accusations of greenwashing. The Global Methane Pledge and emerging disclosure frameworks are putting pressure on industries to act, but progress remains uneven. Companies that lead on methane measurement and reduction not only strengthen their credibility but also unlock opportunities, from carbon markets to reputational advantages with stakeholders.

Ultimately, methane is not just a side issue—it is central to the credibility of net-zero pathways. For oil and gas, agriculture, and waste, ignoring methane metrics means ignoring one of the fastest and most effective levers for slowing climate change. Those who treat it as a priority today will be better positioned in a regulatory and investment landscape that is increasingly unforgiving toward those who do not.

David Miller

Senior Reporter

David Miller focuses on economics trends, analyzing how business, policy, and market developments affect regional and global economies.

World

At least 20 people killed in Russian glide bomb attack on village in eastern Ukraine

Stay focused and remember we design the best WordPress News and

Magazine Themes [...]

Business

Transition vs. Physical Risk A decision tree for which risk dominates by industry.

A decision tree showing whether transition or physical risk is

dominant in each industry based on exposure and vulnerability

[...]

Politics

Getting Assurance-Ready — Controls and evidence trails for sustainability data.

Guidance on creating strong controls and clear evidence trails

to ensure sustainability data is reliable and ready for

assurance reviews. [...]

about us

Venture Hive is your go-to source for sharp insights into the world of business, finance, and

entrepreneurship. We deliver timely news, expert analysis, and thought-provoking stories that keep

you ahead in today’s fast-changing economic landscape.

3 comments

David Bowie

3 hours agoEmily Johnson Cee

2 dayes agoLuis Diaz

September 25, 2025